In November 2024, the Governing Board of the Integrity Council for the Voluntary Carbon Market (ICVCM) approved three methodologies for reducing emissions from deforestation and forest degradation (REDD). The methodologies are now eligible for issuing «high integrity» carbon credits under the Core Carbon Principles (CCPs) label of the ICVCM. We are concerned with this decision. While the methodologies have been improved compared to previous versions, in our assessment they do not meet the requirements of the ICVCM Assessment Framework. Here we explain why.

The ICVCM is a non-profit, independent governance body that aims to set a global standard for high integrity carbon credits. It was founded to build trust in the voluntary carbon market and thereby enable it to scale. In July 2023, the ICVCM published its Core Carbon Principles (CCPs) and an Assessment Framework that establishes requirements that carbon credit categories must meet to qualify for the CCP label. Since then, several carbon crediting programs and methodologies for quantifying emission reductions have been assessed by the ICVCM’s Governing Board as meeting this label.

In its recent decision published on 15 November 2024, the ICVCM Governing Board approved three methodologies for issuing carbon credits from reducing emissions from deforestation and forest degradation:

-

The REDD+ Environmental Excellence Standard (TREES) v2.0, issued by the carbon crediting programme Architecture for REDD+ Transactions (ART), limited to reductions using the TREES Crediting Level Approach and thus excluding the High Forest Cover/Low Deforestation (HFLD) and removals crediting approaches that are still being assessed by the ICVCM.

-

VM0048 Reducing Emissions from Deforestation and Forest Degradation v1.0, issued by the Verified Carbon Standard (VCS) of Verra, limited to avoided unplanned deforestation and projects using version 1.1 of module VMD0055.

-

Jurisdictional and Nested REDD+ (JNR) Framework v4.1, issued by Verra, limited to using VM0048 v1.0 and VMD0055 v1.1 and the JNR Scenarios 2a and 3.

Next to approving these methodologies, the Governing Board published observations on the approval which summarize considerations in the assessment process and identify potential future work of the ICVCM.

We are a group of current and former members of ICVCM Expert Panel and Subject Matter Experts of the ICVCM who have contributed to the development of the ICVCM Assessment Framework. We recognise the urgent need to finance sustainable forest conservation, and observe that the approved methodologies offer improvements over previous versions. However, in their current form, in our assessment they do not meet several requirements of the Assessment Framework. The approval of these methodologies in their current form creates risks to the integrity of the ICVCM and sets a problematic precedent. Here we provide a summary of the main areas where the methodologies fall short of the ICVCM Assessment Framework.

Quantification of emission reductions

Estimating baseline deforestation rates, i.e. how much deforestation would occur in the absence of any REDD mitigation activities, is the biggest challenge in quantifying emission reductions from REDD activities. This is because future deforestation rates depend on a variety of factors, such as pre-existing policies and programs, prices for agricultural and forestry products, or the migration of local deforestation agents. Estimating baseline deforestation levels is therefore subject to large uncertainties.

In assessing methodologies, the ICVCM requires, inter alia, that it is likely that a methodology will not overestimate emission reductions and - if there is still some chance of overestimation from an activity - that it is very unlikely that an activity will significantly overestimate emission reductions. In assessing whether overestimation could occur, all causes of uncertainty should be taken into account (see Table 10.1 of the Assessment Framework). In our assessment, these requirements are not satisfied for the three approved methodologies. The methodologies do not appropriately address the inherent uncertainty in establishing deforestation baselines which can lead to large overestimation for individual mitigation activities.

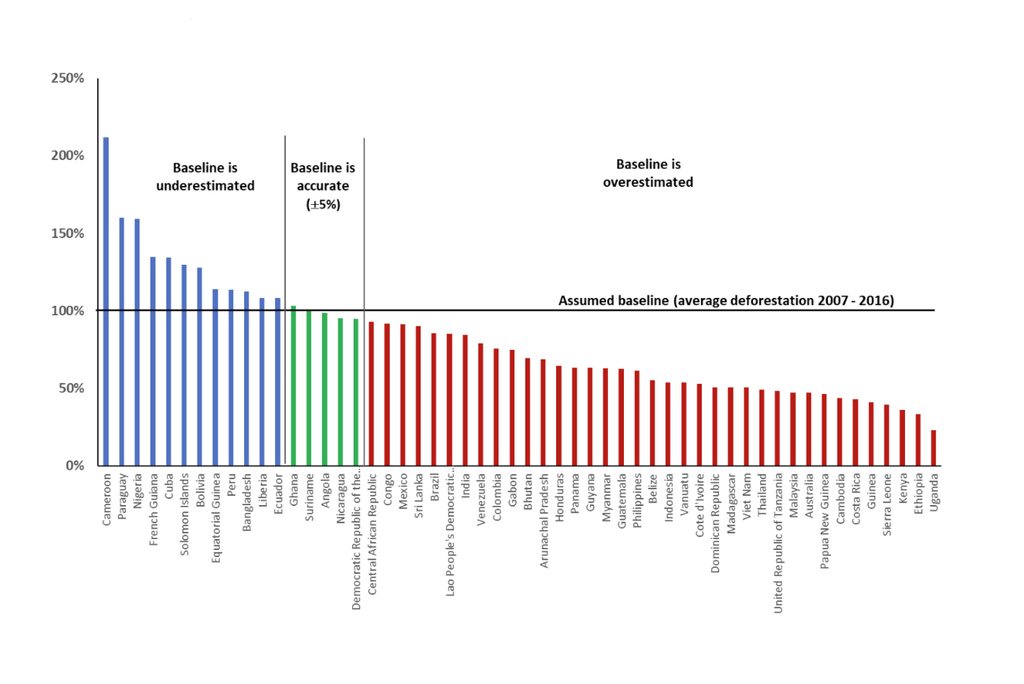

The three methodologies all assume that the average deforestation levels observed in a jurisdiction (e.g. a country or sub-national region) in the past five or ten years will continue in the next crediting or baseline period. As the Governing Board notes in its observations, this can lead to overestimation of baseline emissions in jurisdictions where deforestation levels would decline in the future, and underestimation where they would increase.

This effect is illustrated in the figure below, using historical deforestation data for 54 countries with tropical moist forests. The figure compares actual deforestation levels between two periods: a potential historical reference period used to establish baseline deforestation levels (here 2007 to 2016) and a potential crediting period (here 2017 to 2022). The bars show the deforestation in the crediting period relative to the assumed baseline deforestation derived from the historical reference period (black line). The figure illustrates that the potential for overestimation or underestimation of baseline deforestation rates is very large. In the most extreme case of Uganda, the deforestation in the potential crediting period was only 23% of the deforestation level assumed in the baseline. By contrast, in the case of Cameroon the deforestation in the potential crediting period was 213% of the deforestation level assumed in the baseline. This could lead to large overestimation or underestimation of baseline deforestation rates. We note that this effect may be mitigated over time because the baseline is updated every five to six years. Under ART TREES, however, a jurisdiction may terminate its REDD program without penalty after one baseline period, even if deforestation levels increase again in subsequent periods.

One might argue that underestimation in some jurisdictions or projects would compensate for overestimation in others. In practice, however, the large baseline uncertainty is likely to lead to selection bias. Jurisdictions with declining deforestation trends, or projects within these jurisdictions, may seek carbon credits whereas those with increasing trends are less likely to do so. Even if there is no such active selection, jurisdictions, or projects within jurisdictions, with an overestimated baseline have a competitive advantage, because they receive more carbon credits than their actual emission reductions, while jurisdictions, or projects within jurisdictions, with an underestimated baseline may not move forward or fail because they do not receive sufficient credits to cover their costs. Both effects can lead to more carbon credits being generated from jurisdictions or projects with overestimated baselines, undermining integrity across the portfolio of activities.

The risk of selection bias arises in other ways as well. Under VM0048, the uncertainty of the model used to allocate the jurisdictional deforestation level to specific land areas is not considered. This raises the concern that project areas may be selected based on on-the-ground information about deforestation risk that is not reflected in the model. Furthermore, all of the methodologies provide varying degrees of flexibility on how to quantify carbon stocks. This creates the risk that activity proponents will pick favourable data, assumptions or models that lead to an overestimation of emission reductions. Selection bias has been identified in several studies as one of the major risks in carbon crediting, and could also be a major integrity threat under the approved methodologies.

Due to large unaccounted baseline uncertainty and the considerable risk of selection bias, the methodologies also do not fulfil the requirement of the ICVCM that the credited emission reductions result from the implementation of the mitigation activity and not from changes in exogenous factors that are not related to the mitigation activity (Table 10.6 of the Assessment Framework). Under current rules, the credited emission reductions could partially be generated from changes in factors that are outside the control of the mitigation activity proponents.

Finally, none of the methodologies account for all relevant forms of leakage, as required by the ICVCM (Table 10.5 of the Assessment Framework). In particular, leakage across international borders is not considered but could be significant for some jurisdictions or projects.

Additionality

Emission reductions are only additional if they are caused by the incentives created through carbon credits. Demonstrating additionality is difficult as it requires assessing the counterfactual scenario of what will happen without the carbon credits. Due to the different nature of jurisdictional REDD activities, the ICVCM has separate requirements for such activities (Tables 8.9 and 8.10 of the Assessment Framework). In our assessment, several of these requirements are not fulfilled by the approved methodologies.

The ICVCM requires that jurisdictional activities must submit an implementation plan that identifies and describes the planned new mitigation or enhanced actions (e.g. the introduction of new laws or policies to reduce emissions from deforestation) and to report on their implementation (Table 8.9 of the Assessment Framework). Providing such information is a minimum condition for ensuring that observed lower deforestation levels are caused by new or enhanced mitigation actions, rather than external factors. While ART TREES requires submitting implementations that outline planned programs or activities, it does not require monitoring and reporting on their implementation.

The ICVCM also requires that jurisdictional activities provide evidence that expected revenues from carbon credits (or results-based finance) are decisive for enabling the implementation of the mitigation activities (Table 8.9 of the Assessment Framework). This is important to ensure that expected carbon revenues are a decisive enabler of a jurisdictional activity (i.e., the activity would likely not have been undertaken without this incentive). While the JNR framework explicitly requires this, ART TREES does not have any such provisions.

Finally, the ICVCM requires that carbon crediting programmes shall have provisions that establish a reasonable maximum period between the start date of the mitigation activity and third-party validation or submission of documentation to the carbon crediting programme (Tables 8.3 and 8.10 of the Assessment Framework). Both ART TREES and the JNR framework allow four years to elapse between the start of a jurisdictional activity and the submission of the first documentation (e.g. a concept note). Allowing for such a long period risks granting eligibility to activities that were initially not undertaken with the expectation of generating carbon credits or receiving other types of result-based funding. While what is reasonable may be in the eye of the beholder, we do not believe that four years is sufficiently conservative.

Permanence

Land-use mitigation activities have a risk of non-permanence. Carbon stored as a result of a mitigation activity could be released back into the atmosphere in the future as a result of natural disturbances (e.g. wildfires) or human activities (e.g. harvesting). For activities implemented at jurisdictional scale, such as under ART TREES and JNR, the risk of reversals may be lower than for projects, but still present. For example, under the Zambézia Integrated Landscape Management Program (ZILMP), a jurisdictional approach supported by the World Bank’s Forest Carbon Partnership Facility (FCPF), all previously quantified emission reductions were reversed over 2021 and 2022 when deforestation pressures increased.

For project-scale mitigation activities, the ICVCM requires monitoring and compensation for reversals for at least 40 years, including through the use of a pooled buffer reserve. For jurisdictional-scale mitigation activities, the ICVCM does not require monitoring of reversals over this time horizon. Instead, evidence should be provided that the contributions to a pooled buffer reserve are proportional to the reversal risk and are adequate to compensate for potential reversals over this time frame (section 9 of the Assessment Framework). One of the approved carbon crediting programmes, ART TREES, does not require jurisdictional activities to monitor and compensate for reversals beyond the crediting period. No evidence has been made publicly available by ART TREES that the contributions to the pooled buffer reserve are sufficient to cover reversals over 40 years. As of November 2024, one jurisdiction (Guyana) is registered and 22 are listed under ART TREES. In total, four jurisdictions have submitted monitoring reports. Among these, three have specified a buffer contribution of 5% (Costa Rica, Ghana and Guyana) and one has specified a contribution of 15% (Viet Nam). Given that (i) these contributions are relatively small, (ii) countries can terminate their participation when reversals occur, and (iii) reversal risks can be significant over a 40-year time horizon, we question whether these contributions adequately reflect future reversal risks and will be sufficient to address reversals over this time horizon.

Conclusions

In our assessment, the three approved methodologies do not meet several requirements of the Assessment Framework of the ICVCM. This poses considerable risk for the integrity of the ICVCM and the voluntary carbon market. Given the large size of these activities, we fear that the current methodologies could lead to large volumes of credits not backed by any actual emission reductions. In our view, the methodologies need to be further strengthened to ensure that credited emission reductions are additional and caused by the envisaged mitigation actions.

The authors are current or former members of the Expert Panel of the ICVCM or Subject Matter Experts under the ICVCM. The views in this blog are expressed in their personal capacity. We would like to thank several other experts for their inputs and rich discussions.

Lambert Schneider (Oeko-Institut)

Juerg Fuessler (INFRAS)

Quirin Oberpriller (INFRAS)

Randall Spalding-Fecher (Carbon Limits)

Links: